S&P Global Ratings Expects Kazakhstan’s GDP Growth to Slow in 2026

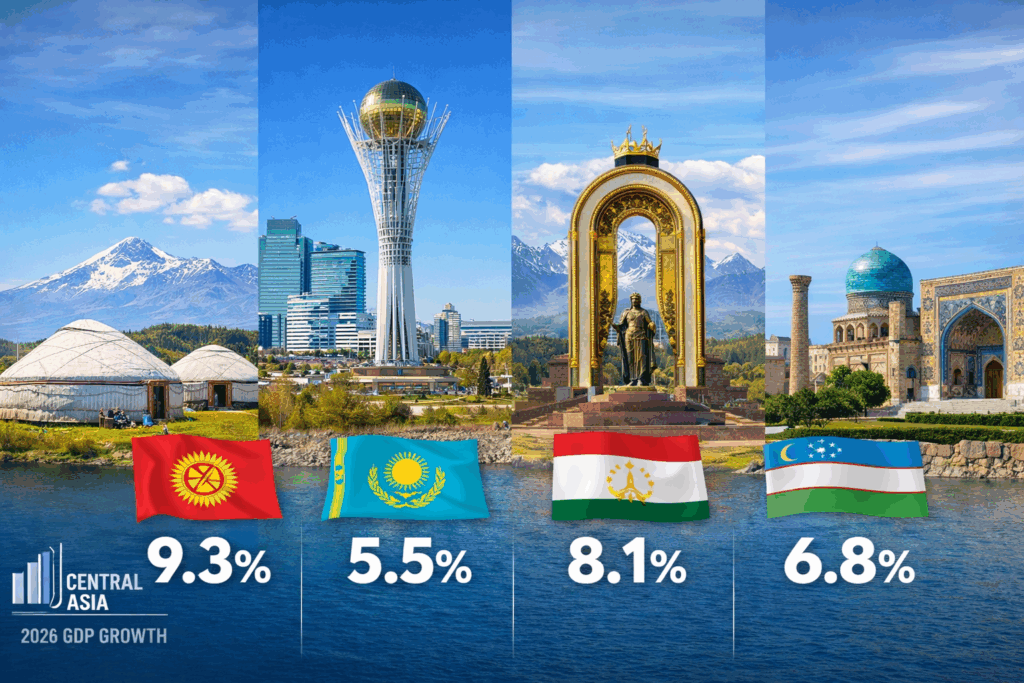

The international rating agency S&P Global Ratings has affirmed Kazakhstan’s long-term sovereign credit rating at BBB- and its short-term rating at A-3, while maintaining a positive outlook on the long-term rating. At the same time, S&P analysts expect economic growth to decelerate in 2026 and warn of persistently high inflation. According to commentary on S&P’s projections by analysts at the Halyk Finance research center, Kazakhstan’s GDP growth is forecast to slow to 4.1% in 2026. The projected slowdown is attributed to a 4% decline in oil production, weaker fiscal stimulus, and reduced consumer activity amid higher taxes and tighter credit conditions. In the medium term, for 2028-2029, S&P expects GDP growth to remain at around 4% or slightly higher. However, risks persist, particularly those related to geopolitical tensions and the continued sensitivity of Kazakhstan’s budget revenues and exports to fluctuations in global oil prices. For comparison, Kazakhstan’s GDP grew by 6.5% in 2025. In 2026, the government expects growth of 6.2%, a notably more optimistic projection than S&P’s estimate. Other international institutions have offered varying forecasts. The European Bank for Reconstruction and Development (EBRD) recently upgraded its 2026 GDP growth forecast for Kazakhstan to 4.7%, up from 4.5%. In contrast, the International Monetary Fund (IMF) in January lowered its 2026 growth forecast by 0.4 percentage points to 4.4%. Returning to S&P’s projections, the agency expects inflation to reach 11% by the end of 2026 and forecasts an exchange rate of 540 tenge per $1. Halyk Finance analysts stated that they broadly agree with S&P’s GDP and inflation forecasts. However, they consider the risks of further weakening of the national currency to be greater than the agency anticipates. According to their estimates, the exchange rate in 2026 could depreciate to 580-590 tenge per $1. S&P also expects the Kazakh government to continue fiscal consolidation in the medium term by expanding the tax base and tightening control over public spending, while preserving substantial liquid reserves. Over the next three years, the government does not plan to withdraw additional funds from the National Fund through targeted transfers or bond placements. The guaranteed annual transfer from the National Fund is set at $5.5 billion, half the $11.1 billion withdrawn in 2025. “We share S&P Global Ratings’ positive assessment, provided that the government strictly adheres to its fiscal consolidation commitments and reduces transfers from the National Fund,” Halyk Finance concluded. The Times of Central Asia previously reported that the IMF believes Kazakhstan’s current GDP growth rate exceeds the country’s long-term economic potential, thereby increasing inflationary pressures and signaling potential overheating of the economy.