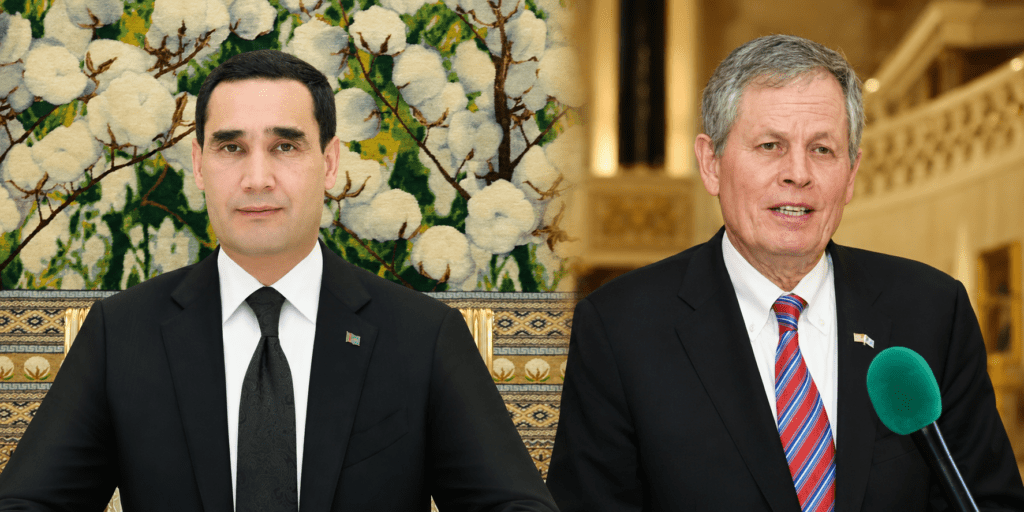

U.S., Turkmenistan Draw Closer with Senator’s Visit to Ashgabat

Turkmenistan wants to deepen cooperation with the United States in areas including fuel and energy, transport, finance, banking, and artificial intelligence, President Serdar Berdimuhamedov has told a visiting U.S. senator. Senator Steve Daines, a Montana Republican who is a leading advocate of U.S.-Central Asia collaboration, also met Gurbanguly Berdimuhamedov, Serdar’s father and powerful predecessor, as well as Foreign Minister Rashid Meredov, in Ashgabat on Thursday. “Our country, endowed with rich natural resources, is implementing a strategy of diversifying energy supply routes and stands for the development of mutually beneficial cooperation based on equal consideration of the interests of producers, consumers, and transit countries,” state media said in a report on the meeting between the president and Daines. Turkmenistan has large natural gas reserves, and China is the primary buyer. Although Turkmenistan is one of the most closed countries in the world, it has been taking steps to expand international contacts and develop its role in the so-called Middle Corridor, a trade network that links China and Europe via Central Asia and has grown in importance during the Russia-Ukraine war. The United States, meanwhile, is building closer ties with Central Asian governments, seeking access to critical minerals and energy, and aiming to reduce Chinese and Russian influence in the region. Daines serves on several Senate committees, including energy and natural resources. He has said he won’t seek re-election this year. Commenting on the senator’s visit, state media in Turkmenistan noted that some major American companies, including Boeing, General Electric, John Deere, and Case New Holland, had been involved in projects in the country for years. U.S. goods trade with Turkmenistan was $152.7 million in 2025, according to U.S. government data. U.S. goods exports to Turkmenistan last year were $113.3 million, up 43.6% from the previous year, and U.S. goods imports from Turkmenistan were $39.4 million, up 169% from 2024. While those numbers are low compared to the volume of trade between the United States and bigger trading partners, the annual percentage increase is notable. A day before his meetings in Turkmenistan, Daines was in Kazakhstan, where he discussed trade and diplomatic ties with President Kassym-Jomart Tokayev. Kazakhstan's leader said he looked forward to traveling to Miami in December to participate in the G20 summit.