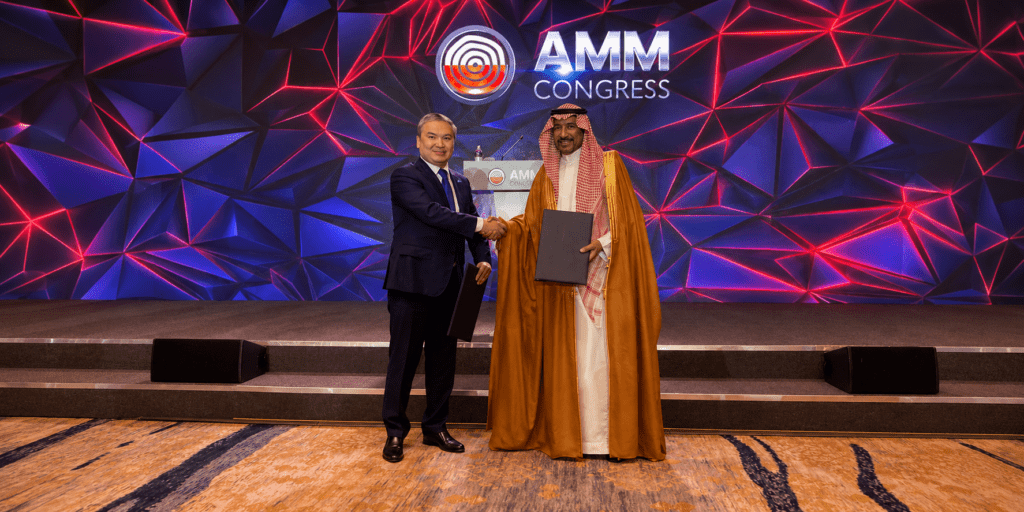

Kazakhstan and Saudi Arabia Sign Mining Cooperation MOU at AMM Congress

ASTANA — Kazakhstan and Saudi Arabia signed a Memorandum of Understanding (MOU) on cooperation in rare earth metals, critical minerals, and the broader mining space at the opening of the Astana Mining & Metallurgy Congress 2026 (AMM) on June 11, marking a significant new step in the two countries’ efforts to expand industrial and critical minerals ties. The MOU was signed by Kazakhstan’s Prime Minister Olzhas Bektenov and Saudi Arabia’s Minister of Industry and Mineral Resources, Bandar bin Ibrahim Al-Khorayef, who arrived in Astana to attend the AMM. The document aims to develop and strengthen cooperation between the Ministry of Industry and Mineral Resources of Saudi Arabia and the Ministry of Industry and Construction of the Republic of Kazakhstan in the field of mineral resources through the exchange of expertise in the mining industry, modern technologies used in mineral resource exploration, and raw materials evaluation. The agreement also covers cooperation across the mining value chain, but with a focus on rare earths and other mineral resources. Both sides are seeking to strengthen collaboration in extraction, processing, and higher value-added production. The signing comes as Kazakhstan is working to attract more investment into critical minerals and downstream processing, while Saudi Arabia is expanding its role in global mining and mineral supply chains as part of its wider economic diversification strategy. Bektenov and Al-Khorayef also held talks in Astana ahead of the congress. According to the Kazakh government, the discussions focused on further cooperation in the mining and metallurgical sectors and in concretizing prospects for joint projects in high-demand and scarce minerals. The sides also discussed investment and trade opportunities as well as geologic mapping and processing, leading to higher value-added production. The signing of the MOU at AMM, considered one of Central Asia’s main mining and metallurgy forums, had a diplomatic dimension at a time when rare earths and critical minerals are moving higher on the agendas of governments and investors. The congress brings together government officials, mining companies, investors, equipment suppliers, and industry experts. For Kazakhstan, the MOU fits into a broader effort to position the country not only as a source of mineral resources, but also as a platform for processing and higher-value production. Astana has been promoting geological exploration, investment in processing capacity, and strategic partnerships with foreign governments and companies. As Kazakhstan seeks to bring more of the value chain onshore, it is building on examples such as titanium production at Ust-Kamenogorsk Titanium and Magnesium and zinc processing at Kazzinc’s integrated facilities. For Saudi Arabia, the agreement reflects Riyadh’s growing interest in international mining partnerships. The Kingdom has been seeking to develop its domestic mineral sector while securing access to strategic raw materials needed for industrial development, clean energy technologies, and advanced manufacturing. At its AMM booth in Astana, Saudi Arabia’s Ministry of Industry and Mineral Resources highlighted its upcoming Future Minerals Forum, set for January 2027 in Riyadh; it is one of the world's leading mining events. Kazakhstan and the other Central Asian countries will be...