Opinion: Central Asia’s Shift from Silk Road Romance to Infrastructure Finance – What the June Forums Are Building

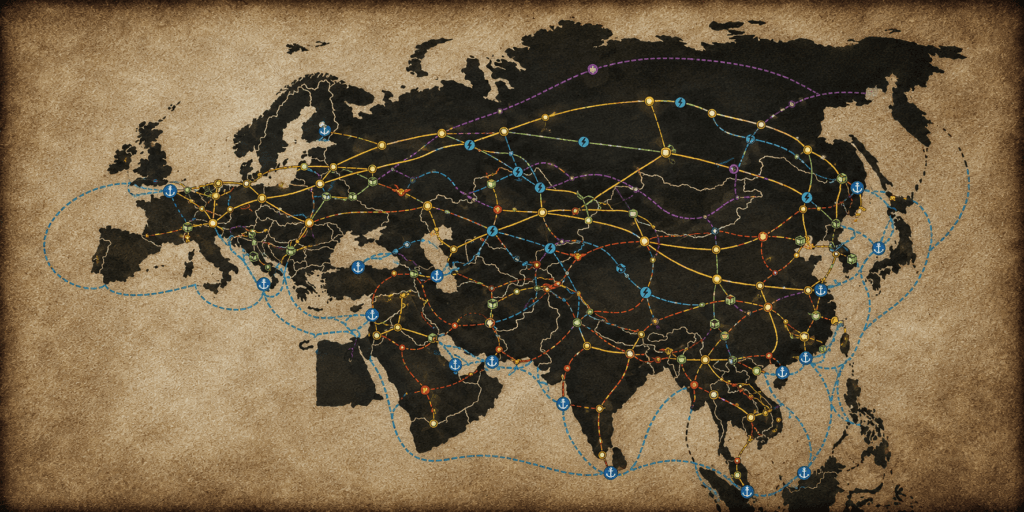

In mid-June, Tashkent and Baku will host two major international finance gatherings within the same regional window: the fifth Tashkent International Investment Forum in Uzbekistan, and the Islamic Development Bank Group’s 2026 Annual Meetings in Azerbaijan. The overlap in timing is useful less as a calendar coincidence than as a signal of how infrastructure, finance, and regional integration are now being discussed together. In Tashkent, the fifth Tashkent International Investment Forum opens under the theme “Investment Resilience: New Frontiers, New Partnerships.” In Baku, the Islamic Development Bank Group will convene delegates from its 57 member countries under the theme “Regional Integration for Sustainable Prosperity.” Add the Astana International Financial Centre’s increasingly active forum calendar, a new cross-border Islamic finance alliance signed in May among regional industry associations, and a stream of connectivity and green investment pledges from recent regional summits, and the wider region looks increasingly focused on turning connectivity talk into investment structures. The more important question is not how much money is being discussed, but what kinds of projects are becoming investable. One answer keeps surfacing: a multi-thousand-kilometer trade route that carries goods from China across Kazakhstan, over the Caspian Sea to Azerbaijan, and onward through Georgia and Türkiye to Europe. The Middle Corridor, formally known as the Trans-Caspian International Transport Route, runs through many of the investment pitches now being made across the region. The forums show how infrastructure, finance, and regional connectivity are increasingly being discussed together. The corridor is one of the clearest tests of whether that agenda can move from conference language into bankable projects. For most of the past century, the world categorized this region under two headings. One is heritage: the caravanserais and blue domes of the old Silk Road. The other is hydrocarbons: the oil and gas beneath the Caspian basin. Both cast the region as a place value came out of or once passed through. The corridor proposes something more ambitious: that value should pass through again, but this time on terms shaped by the region itself. The shift is from selling what lies underground to earning from where the region sits on the map. Freight volumes on the Middle Corridor have risen roughly fivefold over recent years, while transit times have been cut from about a month to roughly two weeks as border procedures and port operations improved. The World Bank’s benchmark study sets out the goal of tripling freight volumes and halving travel time by 2030, and regional projections now point to annual throughput of around ten million tons or more by the end of the decade. For landlocked economies long dependent on a single route to world markets, a second viable artery is less a convenience than a form of strategic insurance. But turning a route on a map into a working corridor requires serious capital. It requires expanded port capacity on the Caspian, additional vessels and ferries, rail upgrades, terminal infrastructure, and the less visible digital and customs systems that allow cargo to clear multiple borders...