Central Asia is entering the critical minerals race at a time when deposits alone no longer confer strategic advantage. The Astana Mining & Metallurgy Congress, scheduled for June 11–12 at Hilton Astana, gives the issue operational form: supply chains, investment, and commercial projects. U.S. Under Secretary Jacob Helberg will participate there and in the preceding C5+1 Critical Minerals Dialogue on June 10–11. The Astana agenda also puts Central Asia’s role in global supply chains directly into view. The test is how quickly governments, investors, and industrial buyers can finance, process, move, and purchase minerals before they are locked into industrial supply chains.

The G7 is moving in the same direction, but through institutional design rather than industrial action. The group is discussing a permanent critical minerals secretariat to maintain continuity across changing G7 presidencies, possibly at either the International Energy Agency or the OECD. The proposal acknowledges a real deficiency in Western coordination, but it also reveals the larger problem: continuity is useful only if it becomes execution. At the same time, reports have circulated about disagreements over stockpiling and leadership, including European resistance to both a single shared stockpile and a U.S.-led structure. For Central Asia, the practical question is not institutional architecture alone, but whether such coordination produces finance, processing capacity, and long-term offtake.

The June dialogue in Astana is part of a wider C5+1 movement from diplomacy toward operational cooperation. Its participants are trying to convert the platform from a talk shop into a vehicle for business transactions. As TCA has reported, U.S. engagement in the region is increasingly tied to business mechanisms, export-credit support, and project finance. Kazakhstan has already moved into this framework track. Kazakhstan and the United States signed a memorandum of understanding on critical minerals cooperation during Tokayev’s November 2025 visit to Washington, and the agreement took immediate shape through the Tau-Ken Samruk–Cove Capital tungsten project. Kazakhstan’s Foreign Ministry later described the MOU as the first agreement of its kind in Central Asia, providing for processing capacity in Kazakhstan, technology transfer, and expanded access for Kazakh products to the U.S. market. In February 2026, Uzbekistan followed with its own U.S. critical minerals track: TCA reported that Tashkent signed a critical minerals MOU on February 4, and that DFC heads of terms for a Joint Investment Framework followed on February 19.

Central Asian governments are not passive terrain for outside competition. Kazakhstan, with Central Asia’s most developed mining and metallurgical base, and Uzbekistan, with a rapidly expanding minerals program, are using minerals competition to attract capital and build processing capacity. They are seeking to diversify partners and move beyond dependence on raw material exports. The regional objective is industrial upgrading while preserving room for maneuver between China, Russia, the United States, Europe, and other partners. The minerals question cannot be separated from the larger Eurasian setting. Central Asia is trying to widen its own field of choice before its options are narrowed by what Hudson Institute senior fellow Ken Moriyasu called, in comments to The Times of Central Asia, a “sanctuary across the Eurasian Heartland.”

The chief constraint is midstream capacity. Western access to Central Asian deposits does not by itself diversify supply chains, because China currently dominates refining and processing. The IEA projects that, by 2035, China will still supply more than 60% of refined lithium and cobalt and around 80% of battery-grade graphite and rare earth elements. Central Asia, therefore, needs additional processing, offtake, and industrial-use channels alongside existing ones. Otherwise, new upstream projects may reinforce today’s downstream concentration: ore mined in one country, concentrated in another, refined through established channels, and returned to global markets without materially widening the region’s commercial options.

Central Asia’s mineral endowment gives the region strategic relevance, but not by itself full supply-chain power. The OECD has identified the region as a veritable periodic table of the elements: it holds significant shares of global reserves in aluminum, chromium, cobalt, copper, lead, manganese, molybdenum, titanium, and zinc. Kazakhstan is the world’s largest uranium producer and Central Asia’s dominant copper producer, while Uzbekistan also has major copper resources and ambitious expansion plans. Kazakhstan, however, is not a greenfield minerals economy. It already has a substantial mining and metallurgical base, including uranium, ferroalloys, copper, zinc, aluminum, titanium, and related industrial infrastructure. The policy question is therefore not whether Kazakhstan can produce minerals, but whether its existing base can be connected to international financing, higher-value processing, and diversified downstream offtake.

Yet the same OECD work points to constraints ranging from exploration and geological-data reporting to state-owned-enterprise dominance, legacy investor concerns, and connectivity. Resource potential becomes investable only when reserves are documented to international standards, transport routes make commercial sense, licensing risks are bounded, and downstream buyers can see a credible industrial path from mine to processor.

Kazakhstan’s tungsten is a case in point. Even as Kazakhstan has moved beyond preliminary interest through a U.S.-linked 70/30 joint venture to develop the North Katpar and Upper Kairakty deposits, recent concentrate exports have still flowed entirely to China. TCA reported that Kazakhstan exported 3,700 tons of tungsten concentrates worth $71 million in 2025, all of it to China.

The case illustrates not a lack of Kazakh industrial competence, but the gap between a major project-development agreement and the still unfinished task of creating diversified processing and offtake channels. At the same time, Cove Kaz has acquired a 70% ownership interest in Severniy Katpar LLP, with Tau-Ken Samruk retaining 30%. The tungsten project is proceeding toward a definitive feasibility study, and U.S. financing agencies have issued letters of interest tied to financing and downstream development. Kazakhstan is also planning new non-ferrous metallurgy projects, including value-added products from copper and aluminum, to expand the value-added role of its existing metallurgical sector.

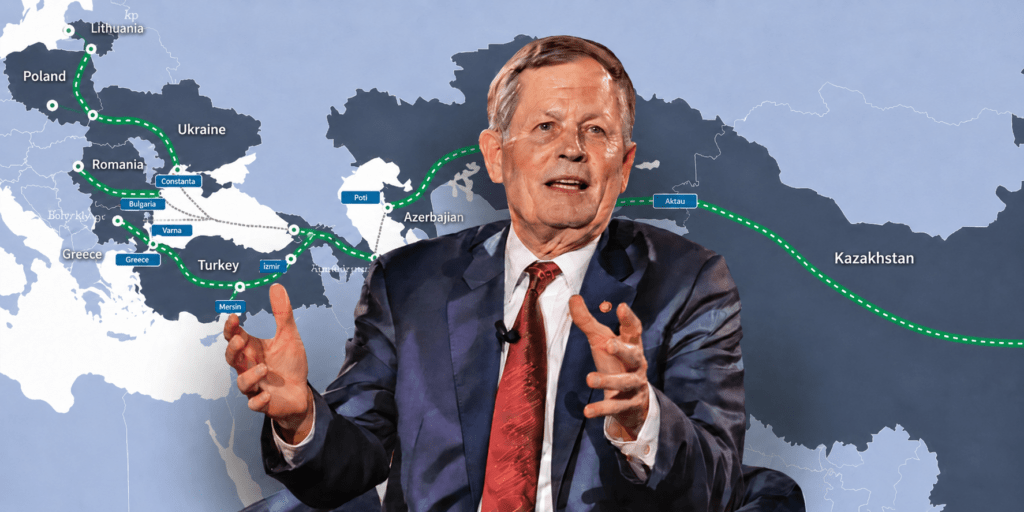

Kazakhstan has promoted the Middle Corridor as part of its offer to U.S. investors, linking mineral development to broader east-west transit capacity while preserving its broader multi-vector approach to connectivity. Critical minerals move through rail systems, Caspian crossings, ports, customs procedures, and offtake contracts. In the same comments, Moriyasu warned that economic, logistical, and security networks can “reinforce each other,” pointing to the risk of path dependency: durable pathways can form before they are recognized as strategic facts.

If midstream control, transit routing, financing habits, and industrial dependency align around one dominant channel, diversification becomes harder even when alternatives remain formally available. For U.S. and European policymakers, critical minerals are therefore part of a wider concern over whether Eurasian connectivity remains open and plural or gradually hardens into what Moriyasu, drawing on U.S. foreign policy scholar Hal Brands, calls “Fortress Eurasia.” For Central Asian governments, the same issue is more immediate and practical: preserving multiple routes, investors, processors, and buyers.

Western partners, therefore, need to move from meetings and secretariats to coordinated finance, processing capacity, and offtake commitments. The proposed G7 unit may preserve institutional continuity. The C5+1 Critical Minerals Dialogue may give the United States and Central Asian governments a working channel. But routes have to be mapped, projects financed, and downstream buyers committed. Only then will Central Asia’s minerals be able to participate in multiple supply chains rather than remain routed primarily through existing concentrated downstream systems. The measure of success will be whether Central Asia can convert critical minerals diplomacy into a growing pipeline of bankable projects that multiply financing, processing, transport, and offtake across the region.

For more on the Astana Mining & Metallurgy Congress and Exhibition 2026, see our special coverage.

This article forms part of The Times of Central Asia’s special coverage of Central Asia’s expanding role in U.S. critical minerals security.