When most people think of the “Silk Road,” they picture a single camel train inching across a tan horizon, blue-white porcelain strapped beside bolts of silk. That fairytale, however romantic, was never true. Medieval Eurasia operated on multiple, overlapping, and improvised routes, often seasonal. And frankly, for a Westerner at the far end, it scarcely mattered how the goods got there, only that they did.

Then, oceanic shortcuts and the Americas rewired global trade; two world wars shattered old geographies, and the Iron Curtain sealed Central Asia into a blank space on Western mental maps. Now, the region is reopening on its own terms, and supply chains are being redrawn in real time. Suddenly, the term “Middle Corridor” has become trendy.

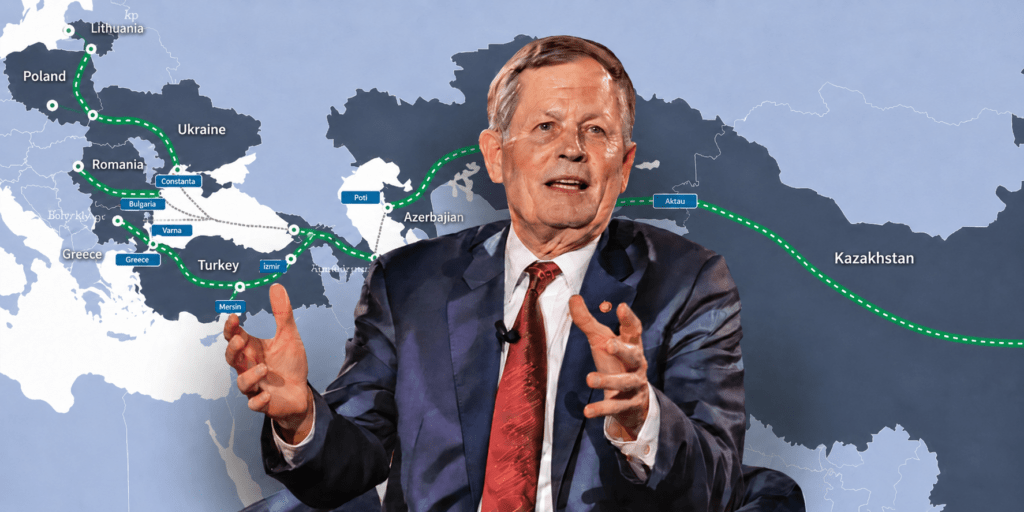

The Caspian Policy Center held its 3rd Trans-Caspian Connectivity Conference in London in July this year, focusing on the theme “Harnessing the Momentum, Building on the Synergies.” The title itself implies a recognition of some “momentum” and some “synergies.” A couple of months after the London conference, I spoke by phone with David Moran, a former UK ambassador with extensive experience in the region, to ask him about what he thinks of the whole “New Silk Road” idea.

His point is refreshingly unsentimental: stop imagining a line and start thinking of it as a web of interconnected channels. In practice, that means folding energy, digital, finance, and steel into a single operating picture so capital shows up on better terms; widening the frame from C5+1 to a Central Asia–South Caucasus–Turkey logic that actually matches how goods and electrons move; and fixing bottlenecks that are more about governance than concrete. We talked about quiet levers: insurance that prices climate risk properly, a digital spine that makes rail and the Caspian behave like one network, and the long-cycle drivers that turn logistics into strategy. Compound those gains, and pretty soon you’ve built something you no longer have to call “alternative.”

“Alternative” lets officials kick decisions into next year; “strategy” forces sequencing, standards in definitions, and capital discipline today. It also resets expectations: this is not a clever detour around trouble, it is the backbone of a regional growth story that European lenders might just actually know how to price.

Seen that way, the geography snaps into focus. On the Caspian, Aktau and Kuryk on one shore and Baku on the other form the hinge, while the BTK railway and Kazakhstan’s Altynkol–Zhetygen pull weight inland. Atyrau is the western Kazakh air node that connects workers, parts and schedules to the Caucasus, the Gulf, and Europe. Thread through the rest: Black Sea power interconnect ideas, subsea data routes, the hydrocarbon pipes already in place. Put it together and you have a web with redundancy, optionality, and recognisable standards built in.

If there’s one real shift, it’s moving from projects to an operating plan. Moran puts it cleanly: “Go for a fully integrated regional connectivity strategy — energy, digital, finance, infrastructure — rather than working through sectoral initiatives separately.” Integration isn’t a slogan; it’s how you cut risk, shorten timelines, and stop term sheets from wobbling. On energy, credibility rises when electrons move as predictably as containers. Caspian port electrification and Black Sea interconnects aren’t side jobs; they’re the ballast that keeps schedules honest.

On digital, build a spine that makes rail and the Caspian behave like one network so customs, dwell times, and inventory are measured, not guessed. Finance sits on top of that stack. “Shadow the EU Gateway processes or the EBRD’s requirements,” Moran says, “and you raise the odds of truly sustainable, forward-looking infrastructure.”

Widen the map, and the logic sharpens. “Central Asia can’t succeed without the South Caucasus, and that means all of it,” Moran told me. “Use all of the corridor. Bring Turkey in. Think C8, even C9.” It is a useful demolition of the photo-op formula that still frames the region as C5 with an ambiguous +1 tacked on. The operating reality is a mesh: Kazakhstan’s rail and ports hinge on Baku; Georgia is the land bridge and the policy signal; Turkey is where the corridor turns into markets.

None of this will surprise readers of S. Frederick Starr, who has argued for decades that Central Asia’s prospects improve when it is managed as an outward-facing system rather than a cul-de-sac. The point is not semantics; it is execution. A C8 or C9 lens forces co-equal planning across Caspian ports, the BTK rail spine, air nodes like Atyrau, and the cables and interconnectors that make the whole thing bankable. You get redundancy, you get pricing power, and, crucially, you get standards convergence without waiting for a Brussels-style treaty.

Moran is clear-eyed about the politics. “You’re not going to get a European-model single market in the Caucasus and Central Asia,” he said. “But you can get closer, bilateral here, trilateral there, and it adds up.” That is why the TITR (Trans-Caspian International Transport Route) machinery, customs pilots, and mutual recognition deals matter more than communiqués. A strategic corridor has to work on an ordinary weekday: staffed borders hitting agreed processing targets, interoperable documents and systems, power, and data that stay up. Get those right and the acronyms fade; reliability is what counts.

The weak points are well known: seasonality on the North Caspian, recurring dredging in Baku, rolling-stock mismatches, and, above all, customs procedures. “Customs harmonisation is the bit everyone underestimates,” Moran told me. “You’re not going to get a single market, but you can get closer, and every hour you shave off adds up.” The remedies are procedural and digital as much as physical: pre-clearance, shared data, mutual recognition, and one-time data entry instead of re-keying at each border. TITR’s working groups exist to convert those fixes from pilots into operating rules rather than press lines.

A quieter lever sits in London, Zurich, and increasingly Almaty: insurance. Central Asian assets face heat, flood, and earthquake risk, yet slow indemnity adjustment can freeze projects when speed keeps timetables intact. The proposition — early-stage but testable — is to hard-wire liquidity via parametric cover, sovereign or municipal pools, and adaptation-linked policies. You do not argue about damage; you pre-agree a trigger: a Syr Darya gauge crosses a level, a Caspian wind station records sustained gusts, a seismic sensor near Almaty hits a ground-acceleration threshold – then funds land within days for dredging, track stabilisation, pier inspections, or border electronics.

This is not theoretical: CCRIF and PCRIC have delivered rapid sovereign payouts; ARC runs an operational African drought pool; Mexico and Jamaica renew parametric catastrophe bonds; Quintana Roo and Hawaii use reef/coastal covers to finance immediate fieldwork. Because payouts are fast and predictable, lenders can treat post-event delays as working capital rather than project risk, lowering the cost of capital up front.

There is a pooled angle too: a cross-border facility for Central Asia and the South Caucasus with first-loss support and global-market reinsurance, while cities buy parametric layers alongside conventional cover and earn premium rebates for pumps, raised substations, or quake-isolation bearings. Very large assets can add resilience bonds or catastrophe tranches that pay on corridor triggers; in Muslim markets, the same logic can sit inside takaful.

None of this works by assertion. Three unglamorous steps matter: data, regulation, and execution. Data means audited sensors, public triggers, and third-party verification to keep basis risk tolerable and disputes rare. Regulation means supervisors and finance ministries that accept parametric wording, pooled schemes, and rapid disbursement that still pass audit. Execution means writing the cover into concessions and loan agreements so the payout flows to the team that fixes the asset, not into a bureaucratic queue.

There is political economy to settle as well: who pays the premium, in which currency, who carries the FX risk, whether a pooled scheme can survive a cross-border spat, who appoints the calculation agent, and how sensors are governed. One messy trigger or corrupted gauge can kill appetite for years. Moran’s view is blunt: “Insurance is being redefined, especially for climate adaptation. Move away from the old models and you can deliver faster.” In this corridor, underwriters are not a footnote to engineers; if pilots prove the cash actually moves when the water rises, they become part of the operating plan.

You cannot run a corridor in the dark. Without a digital spine, plans are promises. The basics are not glamorous: satellite links that keep trains and Caspian ferries visible in real time, fibre at borders so customs is minutes, not guesswork, and uptime targets written into contracts so data availability is an obligation, not a hope. Add a common data model, pre-arrival filings, time-stamped handovers, and an API connection between dispatch, port calls, and border agencies, and the system begins to behave. Moran puts it simply: “It is not one road. It is organic, and it hooks into networks.”

The market is moving that way already. Major cloud players are on the ground: AWS ships Outposts racks to Kazakhstan, has cooperation agreements and pilots with government and local firms, and Kuiper aims to expand satellite connectivity as it rolls out. Do that and the 90th-percentile transit time starts to converge on the median, which is the metric shippers actually remember. Coverage is still patchy in places, but you can start with the busy nodes and publish the service levels so everyone knows what “on time” means.

Strip away the varnish, and the long-cycle driver is minerals. The West needs diversified inputs for batteries, turbines and chips; Central Asia and the South Caucasus sit on rocks that matter. But ore is not a strategy unless it is processed on time and with social licence. “Get it right at the start,” Moran said of mining: governance, water, tailings, consent, traceability. Lead times are unforgiving; shortcuts boomerang. If the corridor wants to be taken seriously, ESG has to move from panel talk to procurement and monitoring, and logistics has to be built for the dull virtue of reliability.

Financing follows that discipline. This is not the age of money spray and ribbon-cuttings. Blended structures and guarantees earn their keep only when they sit on top of cash flows that survive the cycle and on documents lenders recognise. That means a revenue model that is clear about who pays and when: port dues, track access, availability payments, or take-or-pay contracts that tie real counterparties to volumes. It means an SPV with a clean escrow waterfall, maintenance reserves, step-in rights for lenders, and independent O&M with performance KPIs.

It means currency and inflation risk assigned on purpose rather than by accident, with hedging where the tariff cannot bear the shock. And it means environmental and social work that passes on merit, not on charm: proper ESIAs, grievance routes that function, climate-resilience analysis, and reporting that aligns with what European credit committees already read.

The cheapest capital is templated capital. Copy the rulebook and the price falls: EU procurement norms that can survive an audit, EBRD safeguards that are already baked into bank credit manuals, Global Gateway screening so eligibility is not a negotiation. Use public tools to de-risk what actually blocks decisions: UKEF or DFC for political risk and tenor, MIGA for breach-of-contract cover, viability-gap funding where the public good is real but the tariff is capped. Tap instruments investors already buy: green or sustainability-linked bonds for grid and port electrification, sukuk where Islamic finance broadens the buyer base, and local-currency tranches where regulators want domestic participation. Refuse the templates and everything becomes bespoke theatre: long diligence, short tenors, high margins, and a structure no one wants to repeat. Luckily, there are regional initiatives that already have capital attraction as their mandate.

However, there are, of course, familiar ways to foul this up. Over-politicise the corridor and the risk premium rises. Lock into yesterday’s kit and you strand assets before they are depreciated. Treat ESG as choreography and you lose buyers who pay on time. Add a few more own goals and the picture darkens: fragmented standards that make every crossing bespoke; opaque procurement that scares serious lenders; customs “reforms” that fade once the pilot ends; data that is partial, late or siloed; insurance promises that are not embedded in contracts; FX risk left with the party least able to carry it; heroic megaprojects that distract from the small fixes that compound. Ignore maintenance and sensor governance, and you will be back to guesswork the first time the river rises.

If the region can resist those temptations and stick to the dull disciplines that make systems work, 2030 does not need to look heroic. Success is a network that fails rarely and recovers quickly. It is power and data as punctual as containers. It is a minerals chain that is boring in the best possible way because it clears, pays, and repeats.

Or, as Moran put it at the very start of our call: “Don’t wait for big finance or you may miss the boat.” And then the coda that should guide the next few years: “And I think everybody else said much the same thing, it’s there, it’s working, it’s building, but it’s in process.”