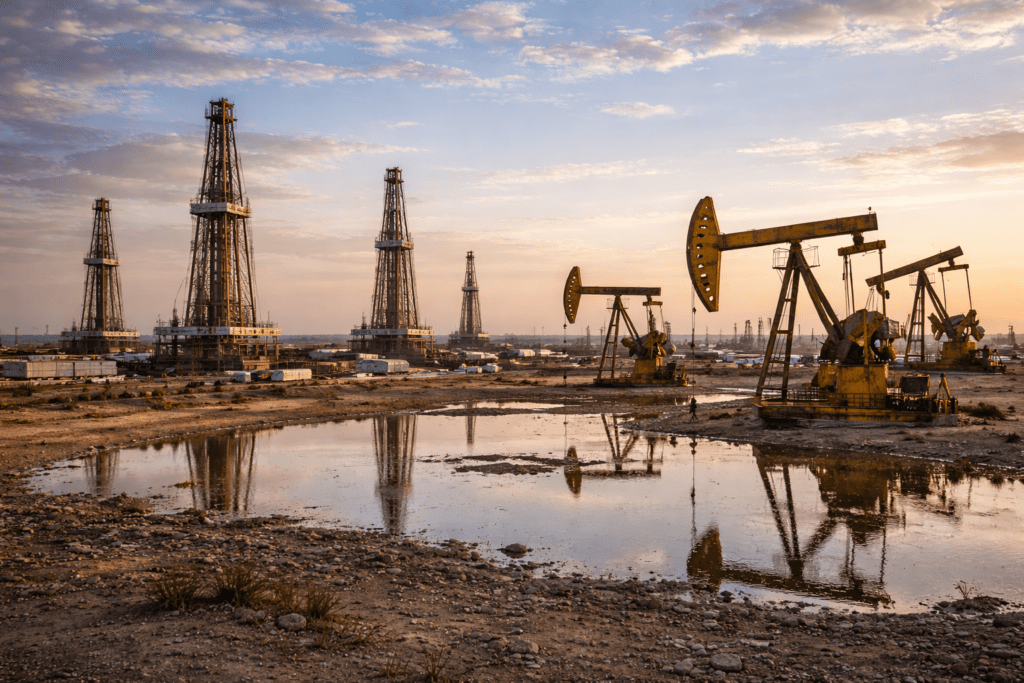

Major Hydrocarbon Field Discovered in Kazakhstan

A major hydrocarbon field has been discovered in Kazakhstan’s Atyrau Region, with reserves potentially comparable to those of the Kashagan oil field, the country’s largest oil source, according to Kurmangazy Iskaziyev, First Deputy Chairman of the Management Board of KazMunayGas.

The site is located on the Zhylyoi Platform near the Caspian Sea coast. Its onshore location could significantly reduce development costs, although the deposits are believed to lie at considerable depths.

Kashagan has long stood as the symbol of both Kazakhstan’s oil wealth and the technical difficulty of extracting it. The offshore field cemented the country’s position as a major crude producer, but also became known for cost overruns, delays, and the engineering challenges of operating in the northern Caspian. Any onshore discovery mentioned in the same breath immediately raises expectations that it could avoid some of those constraints while delivering comparable scale.

Kashagan, discovered in the northern Caspian Sea, remains one of the largest oil fields found globally in recent decades. Its recoverable reserves are estimated at 9–13 billion barrels of oil, with gas reserves exceeding 1 trillion cubic meters. Development is carried out by the North Caspian Operating Company consortium, which includes Shell, TotalEnergies, ExxonMobil, Eni, China National Petroleum Corporation, Inpex, and KazMunayGas.

Speaking at the Geoscience & Exploration Central Asia forum, Iskaziyev said the resource potential of the Zhylyoi Block, including Karaton, Kazhygali, and Zhylyoi, is estimated at 4.7 billion tons, with total geological potential reaching up to 20 billion tons of oil equivalent.

At this stage, such figures reflect geological potential rather than proven, recoverable reserves. In Kazakhstan, as elsewhere, moving from estimate to production depends on depth, pressure, sulfur content, and the cost of drilling and processing. Large discoveries can take years to confirm commercially, particularly in high-pressure or technically complex formations.

KazMunayGas has already begun exploration work. A well 5,750 meters deep has been drilled at the Karaton site, and five promising targets have been identified as part of a joint project with Tatneft. During testing at one of these sites, a gas flow containing hydrogen sulfide was recorded.

The main challenge remains the depth of the deposits, which may reach up to 9 km. According to Iskaziyev, these conditions are comparable to projects undertaken by KazMunayGas’s Chinese partners, including Sinopec and China National Petroleum Corporation, where drilling depths can reach up to 11 km.

The company plans to expand geological exploration into neighboring areas, including Kazhygali, and is negotiating subsoil use contracts.

The timing is significant. Kazakhstan is under growing pressure to demonstrate that its oil sector can still deliver major new projects as existing fields mature. A large onshore discovery in Atyrau would reinforce the region’s role as the core of the country’s energy system and support efforts to sustain export volumes and investor interest.

At the forum, a memorandum of understanding was also signed between KazMunayGas and BP on cooperation in geological exploration and the development of the Ustyurt Block in the Mangistau Region.

The Times of Central Asia previously reported that Kazakhstan is involved in an international arbitration dispute with the North Caspian Operating Company consortium over environmental issues related to the Kashagan project.

That dispute reflects a broader pattern. Kazakhstan’s experience with Kashagan shows that giant oil projects rarely develop smoothly. The field brought vast reserves but also years of delays, technical setbacks, and regulatory friction. That legacy is likely to shape how officials and investors approach any new discovery presented as a potential peer to the country’s largest oil asset.