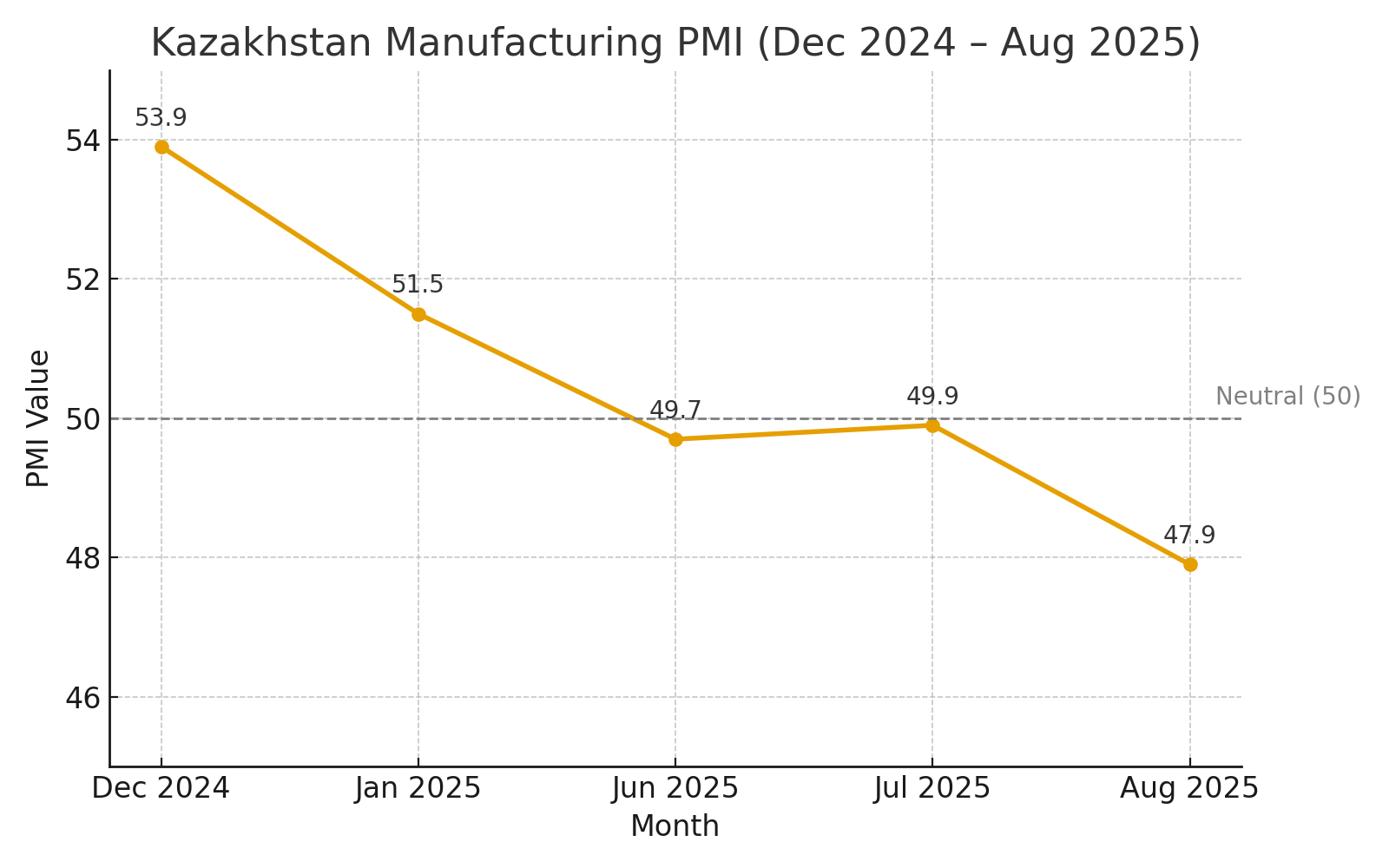

Kazakhstan’s manufacturing sector slipped further in August, with the latest Purchasing Managers’ Index (PMI) falling to 47.9. That was down from 49.9 in July and 49.7 in June, keeping the index below the neutral 50 mark for a third straight month. It also marked the sharpest deterioration in manufacturing activity since March 2022, according to S&P Global and Freedom Holding Corp.

From Highs to Lows

The striking downturn comes on the heels of a banner year. In December 2024, the PMI reached a record 53.9, capping 11 straight months of expansion. Buoyed by post-pandemic recovery and government support, manufacturing output grew by 6.8% in 2024, the fastest pace since 2011, helping push GDP growth to 5%.

But momentum cooled as 2025 began. The PMI slipped to 51.5 in January, reflecting slower expansion after the year-end surge. By June and July, it hovered just under 50, signaling stagnation. Seasonal shutdowns for repairs in August contributed to weaker output, but analysts say the slide points to deeper structural pressures.

Kazakhstan’s PMI peaked at 53.9 in December 2024 but slid steadily through 2025, falling into contraction territory below 50 by mid-year and hitting 47.9 in August — the sharpest deterioration since March 2022.

Orders Dry Up, Costs Rise

The August report revealed broad-based weaknesses. New orders fell for the first time in 19 months, ending a growth streak that began in early 2024. The decline reflected lower demand from both domestic and export markets. With fewer orders, factories scaled back staffing and cut input purchases.

At the same time, costs surged. A weak tenge and fuel inflation made imports more expensive, while logistics delays lengthened supplier delivery times. These pressures forced firms to raise output prices at a faster pace, risking competitiveness.

“August saw another sharp decline in business activity in Kazakhstan’s manufacturing sector,” said Yerlan Abdikarimov of Freedom Finance Global, which partners with S&P on the survey. He cited weak demand, volatile commodity markets, rising costs, and currency and tax pressures.

Taxes have indeed become a burden. A new code passed in mid-2025 raised the extraction royalties on metals, hitting downstream metallurgy. Inflation stood at 12.2% in August 2025, with the National Bank keeping its policy rate high at 16.5% in a bid to tame prices. That leaves financing costly for businesses, resulting in squeezed margins and thinning confidence. The August survey showed business confidence at its lowest since 2021. While firms still expect growth over the next year, their optimism is increasingly cautious.

Industry Responses and Government Initiatives

Some executives see hope in the government’s industrial policy. A $400 million cotton-to-textile cluster is under construction with Chinese partners in Turkestan, aiming to process domestic cotton into textiles at scale. Officials say the project, due to start production by late 2025, will create thousands of jobs and expand exports. Light industries, such as textiles and apparel, posted strong growth in the first half of 2025, with clothing up about 5.6% and textiles 5.7% according to official data. Chemicals and construction materials also expanded, though these gains risk being overshadowed if the overall PMI remains in contraction.

In the meantime, many companies appear to be conserving cash and pushing for reforms such as tax relief or export incentives. The government has emphasized macro stability while promoting diversification projects, a balancing act that may not provide immediate relief.

Regional Comparisons

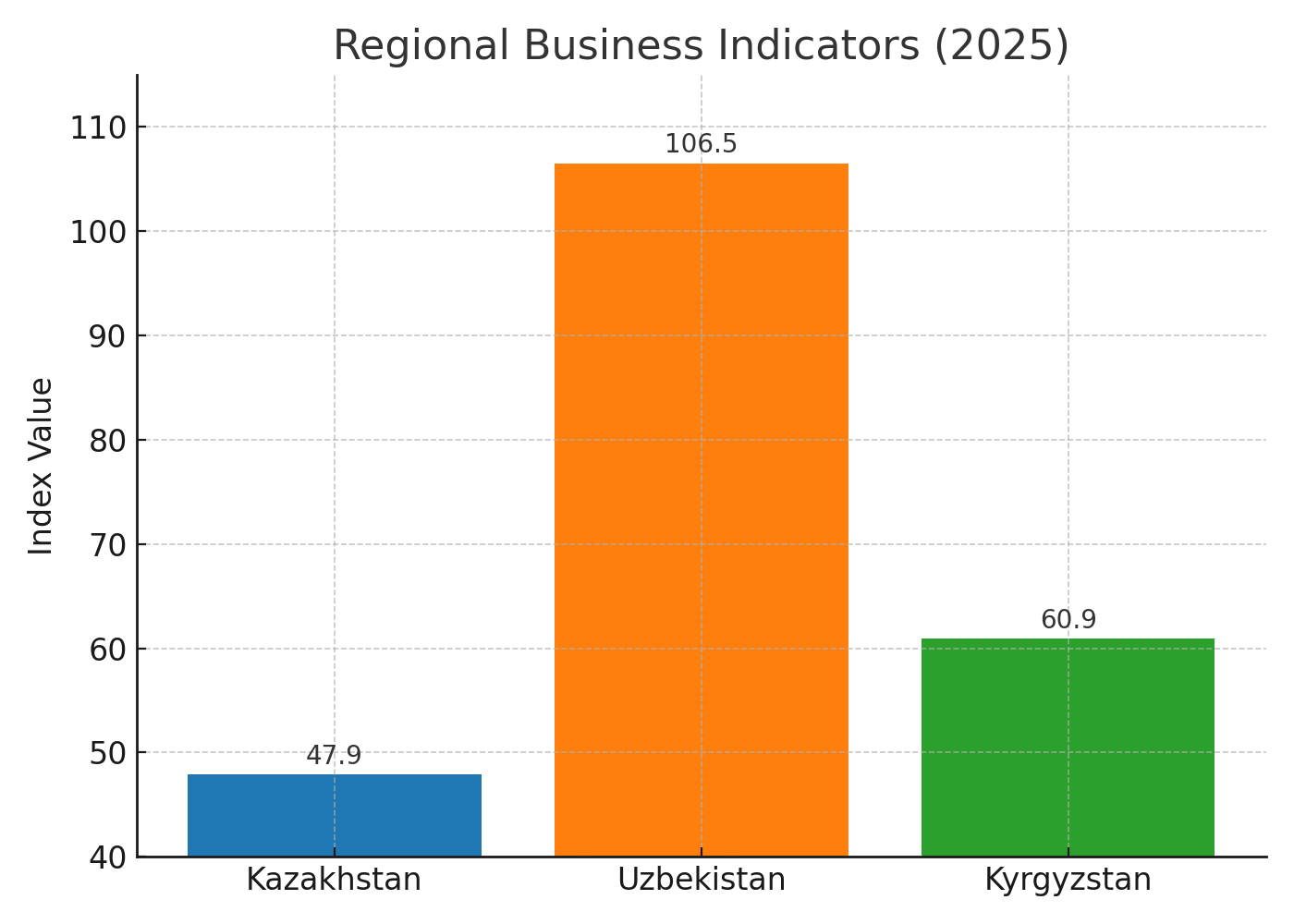

Kazakhstan’s struggles stand out in the region. Uzbekistan reported its industrial sector grew by about 6.5% in the first quarter of 2025, as overall GDP rose 6.8% year-on-year, while forecasts for the year remain firm at around 6.5–6.7% growth. Construction, services, and exports have been expanding, with the Center for Economic Research and Reforms reporting that Uzbekistan’s Business Activity Index jumped 15.9% in July 2025 and a further 2.9% in August, indicating sustained momentum.

Kyrgyzstan has also reported robust growth, with its composite business-activity index rising to 60.9 in spring 2025, powered by strong performances in agriculture, trade, and services. While not a pure manufacturing PMI, the index signals broad economic momentum and underscores the contrast with Kazakhstan’s manufacturing downturn.

Kazakhstan’s PMI of 47.9 contrasts with Uzbekistan’s 6.5% industrial growth index (106.5) and Kyrgyzstan’s business activity index of 60.9, highlighting the country’s relative slowdown compared with its Central Asian neighbors.

The difference lies partly in structure. Kazakhstan’s manufacturing is heavily tied to metals and heavy industry, leaving it vulnerable to global price swings and taxes, while its neighbors benefit from more diversified or service-led growth. This structural gap means that while Kazakhstan’s factories are exposed to volatility in commodities; over half of its exports are oil-based, while its neighbors are seeing growth driven more by services, construction, and manufacturing, which smooths out external shocks.

Outlook: Balancing Risk and Opportunity

The International Monetary Fund projects Kazakhstan’s GDP growth at 4.9% in 2025, backed by strong mining and industrial output. Government plans include implementing 190 new industrial projects in 2025 worth about 1.5 trillion tenge ($2.78 billion) and expected to create more than 23,000 permanent jobs, with dozens already launched in metallurgy, chemicals, and special economic zones. Services and construction also remain resilient, helping to offset pressure in manufacturing. External conditions may provide some relief: global commodity prices have steadied, and the tenge regained ground in early September. A rebound in Russian or Chinese demand could also support factory orders.

Despite weak PMI readings, recent macro data paints a more nuanced picture. Industrial output expanded by 6.9% in the first seven months of 2025, driven by mining and manufacturing. Mining expanded 8.5% in the first seven months of 2025, though there are indications that growth could moderate later in the year. Overall GDP grew by 6.5% through the first eight months of 2025, supported by trade, industry, construction, and services. At a policy level, the government has introduced a Register of State Support Measures with over 100 tools to assist businesses, while reforms to special economic zones and new investments in rare-earth production reflect efforts to diversify and add value.

Significant risks remain, however. Persistently high inflation could keep borrowing costs elevated, limiting investment, while any downturn in global markets would weigh on exports. Analysts caution that recovery will depend on stabilizing the macroeconomic environment and ensuring that planned projects move from blueprints to production.

For now, the August PMI data serves as a wake-up call. A sector that was expanding just months ago is now under pressure from weaker demand, rising costs, and tighter financing. Kazakhstan’s path forward will depend on whether policymakers can restore stability while accelerating diversification, turning long-term industrial plans into real output gains.