Central Asian governments are racing to protect citizens and keep trade moving as the U.S.–Israel war with Iran widens across the Middle East, disrupting airspace and driving up shipping and energy costs. The effects of the conflict are reaching a region that has spent the past four years trying to diversify trade routes and reduce dependence on maritime chokepoints, now disrupted by rising risk and transport volatility.

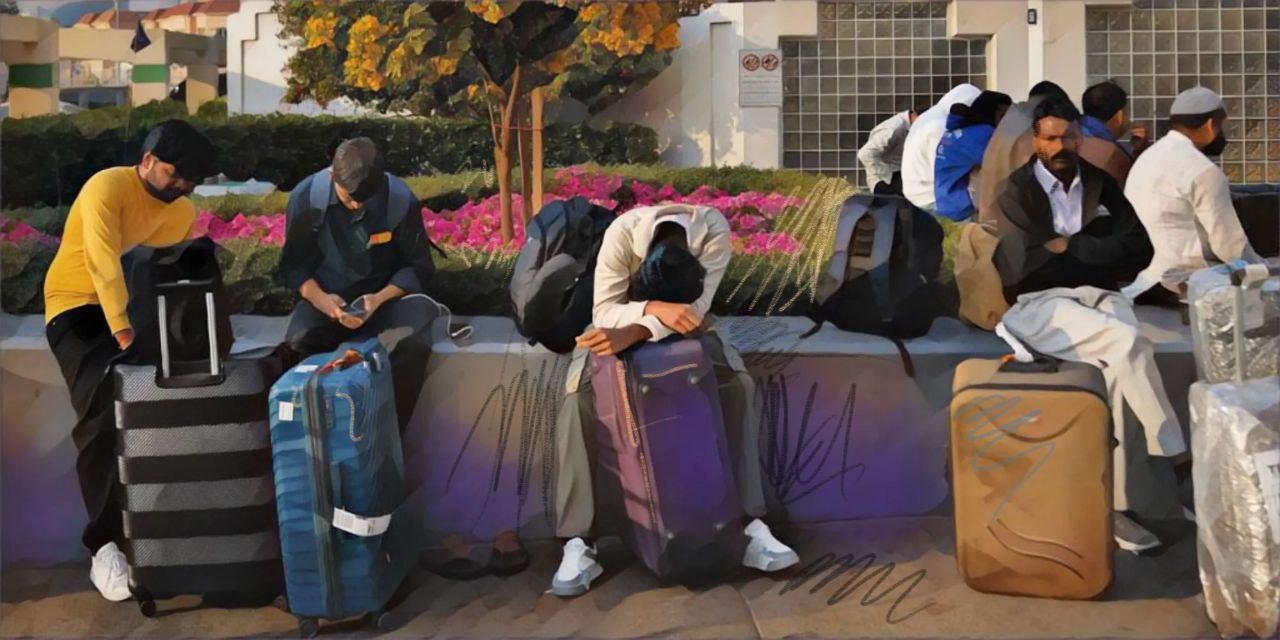

The threat to its citizens has become immediate for Central Asian governments. On March 1, Kazakhstan’s Foreign Ministry said that it was working on evacuation measures for its nationals in escalation zones and urged citizens to follow official updates from diplomatic missions. It also advised Kazakh citizens in Iran to explore overland exits, including via Azerbaijan, Armenia, Türkiye, and Turkmenistan, given airspace closures and flight suspensions. Uzbekistan’s Foreign Ministry issued safety guidance for citizens in the United Arab Emirates, urging them to avoid crowded areas and adhere to official security directives as tensions in the region escalated. Tajik nationals have already been among those leaving Iran through Azerbaijan’s Astara crossing, with The Times of Central Asia reporting yesterday that five civilians from Tajikistan are among foreigners from numerous countries who have crossed from Iran into Azerbaijan.

For Central Asia, the crisis is hitting both its people and its trade routes. The same border crossings used for evacuations sit on corridors that carry freight and connect the region to southern markets. Azerbaijan’s role as a transit hub has grown sharply over the past decade, but in this crisis, it is also a pressure valve for land exits from Iran. As of March 2, more than 300 people have been evacuated from Iran via Azerbaijan. Any tightening at borders or disruptions to rail and road links around the Caspian immediately affect how Central Asian states move both people and cargo.

Oil and shipping costs are rising sharply. On March 1, oil prices jumped by around 10%, with analysts warning prices could move toward $100 a barrel if disruption in the Strait of Hormuz worsens. The impact across Central Asia has been uneven. Kazakhstan may see stronger export revenues in the short term due to higher crude prices, but that gain comes with volatility and increased import costs across the region. ING stated that stronger commodity prices could improve the external balance of fuel exporters such as Kazakhstan, while increasing inflation risks for importers.

Shipping poses a deeper structural risk. Tanker owners and traders have slowed or suspended transits through the Strait of Hormuz because of security fears and insurance constraints, even without a formal blockade. Higher risk premiums feed directly into freight rates on the routes Central Asian exporters use to reach Europe, the Gulf, and South Asia. When insurers reprice war risk, smaller shippers and landlocked economies absorb the cost first.

Iran is central to Central Asia’s trade geography. It serves as a transit state for the southern corridor linking Central Asian rail and port networks to Türkiye, Europe, and the Gulf. Central Asian capitals see Iranian ports as a gateway to the Persian Gulf and Indian Ocean and a way to diversify export routes beyond northern corridors, even as they assess cost, risk, and political uncertainty in the region. Turkmenistan, which borders Iran and anchors much of this routing, has continued talks with Tehran on rail connectivity, including discussions in Sarakhs that Iranian media described as strategic for transit corridors.

The strain is also visible in aviation. Airspace closures and hub disruptions have forced airlines to reroute or cancel flights, cutting cargo capacity and raising costs for high-value goods that usually move by air. As shipments shift to land and sea, congestion has increased at rail terminals and ports used by Central Asian supply chains. Exporters of perishables, time-sensitive components, and precious metals are facing immediate exposure.

Central Asia has spent several years building alternative routes, including the Trans-Caspian corridor, also known as the Middle Corridor. An OECD report from November 2025 on Kazakhstan’s segment of the Corridor documented rising sea cargo volumes and the need to upgrade port infrastructure to sustain growth. Rising Gulf instability increases pressure on this route; greater freight diversion toward Eurasian land corridors would intensify congestion at Caspian ports, strain ferry capacity, and slow border processing.

Transport planning now intersects directly with geopolitics. On February 19, President Donald Trump convened the inaugural meeting of the Board of Peace in Washington, presented as a reconstruction and coordination mechanism for Gaza and backed by member states, including Kazakhstan and Uzbekistan. The expansion of the conflict with Iran has heightened security pressure across the Gulf and increased uncertainty for trade and finance. For Central Asian governments, the latest events underscore how quickly U.S. policy shifts can alter sanctions exposure, banking access, and the risk profile of routes that pass through Iran or Gulf markets.

Policymakers face a difficult choice. The southern corridor through Iran offers shorter access to warm-water ports and Türkiye’s logistics network. The war increases the risk of sudden border restrictions, rail disruption, or expanded sanctions that complicate financing and insurance. The Middle Corridor avoids Iran, but depends on Caspian maritime capacity and stable conditions in the South Caucasus. Both routes face heightened uncertainty as the conflict widens.

For ordinary Central Asians, the first concern is safety: embassy hotlines, cancelled flights, and overland exits from Iran and neighboring states. The second is cost. Sustained high oil prices and elevated freight premiums push up food and consumer prices. Countries reliant on imported fuel or staples are especially vulnerable. Major infrastructure projects across the region remain under construction and depend on predictable transit conditions to deliver returns.

Redundancy in trade and transport routes has become essential. Multiple corridors are no longer a future ambition but a requirement for economic stability and public safety.

– Explore our complete Gulf crisis timeline, bringing together every major development and its implications for Central Asia in chronological order.